Enterprise Risk Management Formula Book

Appendix A.2: Probability Distributions:

Continuous (univariate) distributions (b) exponential, F, generalised extreme

value (GEV) (and Frechét, Gumbel and Weibull)

[this page | pdf]

Distribution name

Exponential

distribution

|

|

Common notation

|

|

|

Parameters

|

= inverse

scale (i.e. rate) parameter ( = inverse

scale (i.e. rate) parameter ( ) )

|

|

Domain

|

|

|

Probability density

function

|

|

|

Cumulative distribution

function

|

|

|

Mean

|

|

|

Variance

|

|

|

Skewness

|

|

|

(Excess) kurtosis

|

|

|

Characteristic function

|

|

|

Other comments

|

Also called the negative exponential distribution.

The mode of an exponential distribution is 0. The exponential distribution

describes the time between events if these events follow a Poisson process.

It is not the same as the exponential family of distributions. The quantile

function, i.e. the inverse cumulative distribution function, is  . .

The non-central moments ( are are

. Its

median is . Its

median is  . .

|

|

Distribution name

|

F distribution

|

|

Common notation

|

|

|

Parameters

|

= degrees

of freedom (first) (positive integer) = degrees

of freedom (first) (positive integer)

= degrees

of freedom (second) (positive integer) = degrees

of freedom (second) (positive integer)

|

|

Domain

|

|

|

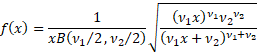

Probability density

function

|

|

|

Cumulative distribution

function

|

|

|

Mean

|

|

|

Variance

|

|

|

Skewness

|

|

|

(Excess) kurtosis

|

|

|

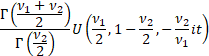

Characteristic function

|

Where  is the

confluent hypergeometric function of the second kind is the

confluent hypergeometric function of the second kind

|

|

Other comments

|

The F distribution is a special case of the Pearson

type 6 distribution. It is also known as Snedecor’s F or the

Fisher-Snedecor distribution. It commonly arises in statistical tests linked

to analysis of variance.

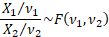

If  and and  are

independent random variables then are

independent random variables then

The F-distribution is a particular example of the

beta prime distribution.

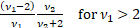

The mode is  . There is

no simple closed form for the median. . There is

no simple closed form for the median.

|

|

Distribution name

|

Generalised extreme

value (GEV) distribution (for maxima)

|

|

Common notation

|

|

|

Parameters

|

= shape

parameter = shape

parameter

= location

parameter = location

parameter

= scale

parameter = scale

parameter

|

|

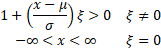

Domain

|

|

|

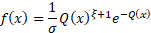

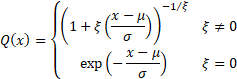

Probability density

function

|

where

|

|

Cumulative distribution

function

|

|

|

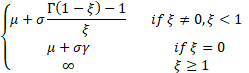

Mean

|

where  is Euler’s

constant, i.e. is Euler’s

constant, i.e.

|

|

Variance

|

Where

|

|

Skewness

|

where  is the

Riemann zeta function, i.e. is the

Riemann zeta function, i.e.  . .

|

|

(Excess) kurtosis

|

|

|

Other comments

|

defines

the tail behaviour of the distribution. The sub-families defined by  (Type

I), (Type

I),  (Type II)

and (Type II)

and  (Type III)

correspond to the Gumbel, Frechét and Weibull families respectively. (Type III)

correspond to the Gumbel, Frechét and Weibull families respectively.

An important special case when analysing threshold

exceedances involves  (and

normally ) and this

special case may be referred to as (and

normally ) and this

special case may be referred to as  . .

|

NAVIGATION LINKS

Contents | Prev | Next