Calculating TVaR if a distribution has a

quantile-quantile form (versus the normal distribution) that is a cubic

polynomial

[this page | pdf | references | back links]

A method that some practitioners use to estimate risk

measures such as Value-at-Risk

(VaR) and Tail

Value-at-Risk (TVaR) for fat-tailed distributions is make use of the

Cornish-Fisher asymptotic expansion, see derivation of the

Cornish-Fisher expansion or MnCornishFisher4.

This is a methodology for predicting the shape of a (univariate) distributional

form merely from the moments of the distribution, most commonly merely its

mean, standard deviation, skew and (excess) kurtosis.

However, Kemp (2009) notes

that the Cornish-Fisher approach has some undesirable features including not

necessarily giving appropriate weight to different parts of the distributional

form. In effect it can result in estimation of outlying quantiles of the

distribution more from the distributional shape in the centre of the

distribution than from its shape in its tails, which is counterintuitive and

liable to error. Kemp proposes a more empirical approach in which the

distributional form and hence the risk measure is derived from a curve that is

directly fitted to the shape of the quantile-quantile plot, possibly giving

greater weight to observations in this curve fitting process to regions of the

distribution that the user is most interested in analysing. His suggested curve

form to use for this purpose is a cubic, since the fourth moment Cornish-Fisher

approach is in effect also characterised by a cubic quantile-quantile plot but

not necessarily one giving the most suitable weights to different parts of the

distributional form.

As noted in Kemp (2009)

such an approach also simplifies computation of TVaR risk measures.

Suppose the quantile-quantile plot (versus the corresponding

standardised normal distribution) takes a cubic form, i.e. is of the form  . Not

all choices of

. Not

all choices of  correspond

to a valid probability distribution. Real vaued probability distributions must

have monotonically non-decreasing cumulative distribution functions, which in

this instance means that

correspond

to a valid probability distribution. Real vaued probability distributions must

have monotonically non-decreasing cumulative distribution functions, which in

this instance means that  needs

to be non-decreasing for all

needs

to be non-decreasing for all  ,

which requires

,

which requires  and

and  .

.

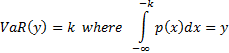

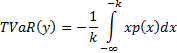

If the cubic does correspond to a valid probability

distribution then the VaR and TVaR of the distribution, for a given confidence

level  , are

defined as follows, where

, are

defined as follows, where  is

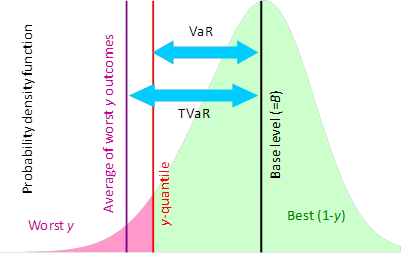

the distribution’s probability density function (assuming that we adopt the

same definition for TVaR as is used in the illustrative chart below and

suitably rebase the -axis,

i.e. here set

is

the distribution’s probability density function (assuming that we adopt the

same definition for TVaR as is used in the illustrative chart below and

suitably rebase the -axis,

i.e. here set  ):

):

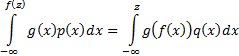

At first sight these integrals look quite complicated to

evaluate, since they appear to require us to derive .

However we note that in this instance the following relationship applies for an

arbitrary  satisfying

appropriate regularity conditions, where

satisfying

appropriate regularity conditions, where  is

the probability density function of the corresponding normal distribution

(with, say, mean

is

the probability density function of the corresponding normal distribution

(with, say, mean  and

standard deviation

and

standard deviation  ) and

) and

is

the standard inverse normal

function:

is

the standard inverse normal

function:

VaR corresponds to the case where  ,

i.e. can be evaluated, as we might expect as:

,

i.e. can be evaluated, as we might expect as:

TVaR corresponds to the case where  ,

i.e.

,

i.e.  and

thus can be derived analytically (as a function of

and

thus can be derived analytically (as a function of  , and

deeming to

be ‘analytic’) using methodologies set out in integrating

piecewise polynomials against a Gaussian probability density function.

, and

deeming to

be ‘analytic’) using methodologies set out in integrating

piecewise polynomials against a Gaussian probability density function.