Stable Distributions

3. Other features

[this page | pdf | references | back links]

Return

to Abstract and Contents

Next

page

3.1 Three special cases of stable laws, which have

closed form expressions for their probability densities are:

(a) Normal (i.e.

Gaussian).  if

if  has

density

has

density

(b) Cauchy.  if has

density

if has

density

(c) Levy.  if has

density

if has

density

3.2 Generic features of stable distributions noted

by Nolan

(2005) include:

(a) They are unimodal

(b) When  is

small then the skewness parameter is significant, but when is

close to 2 then it matters less and less.

is

small then the skewness parameter is significant, but when is

close to 2 then it matters less and less.

(c) When  (i.e.

the Normal distribution), the distribution has ‘light’ tails and all moments

exist. In all other cases (i.e.

(i.e.

the Normal distribution), the distribution has ‘light’ tails and all moments

exist. In all other cases (i.e.  ), stable distributions

have heavy tails and an asymptotic power law (i.e. Pareto) decay. The term stable

Paretian is thus used to distinguish the

), stable distributions

have heavy tails and an asymptotic power law (i.e. Pareto) decay. The term stable

Paretian is thus used to distinguish the  case

from the Normal case. A consequence of these heavy tails is that not all population

moments exist. If then the population

variance does not exist, and if

case

from the Normal case. A consequence of these heavy tails is that not all population

moments exist. If then the population

variance does not exist, and if  then the population mean

does not exist either. Fractional moments, e.g. the

then the population mean

does not exist either. Fractional moments, e.g. the  ’th

absolute moment, defined as

’th

absolute moment, defined as  ,

exist if and only if

,

exist if and only if  (if ). Of

course all sample moments exist, if there are sufficient observations in

the sample, but these may exhibit unstable behaviour as the sample size

increases if the corresponding population moment does not exist.

(if ). Of

course all sample moments exist, if there are sufficient observations in

the sample, but these may exhibit unstable behaviour as the sample size

increases if the corresponding population moment does not exist.

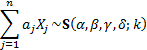

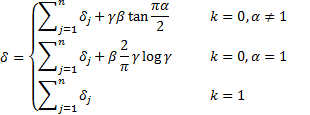

3.3 Linear combinations of independent stable

distributions with the same index, , are stable. If  for

for  then

then

where:

In this generalisation of the definition of stable

distributions given in Section 1.3 it is

essential for the ’s to be the same. Adding

stable random variables with different ’s

does not result in a stable law.

NAVIGATION LINKS

Contents | Prev | Next