Estimating operational risk capital

requirements assuming data follows a bi-uniform or a triangular distribution

(using maximum likelihood)

[this page | pdf | back links]

Suppose a risk manager believes that an appropriate model

for a particular type of operational risk exposure involves the loss,  ,

never exceeding an upper limit,

,

never exceeding an upper limit,  ,

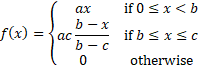

and the probability density function

,

and the probability density function  taking

the form of a bi-uniform distribution:

taking

the form of a bi-uniform distribution:

where  are

all constant.

are

all constant.

Suppose we want to estimate maximum likelihood estimators

for  ,

,

and

and

given

losses of

given

losses of  ,

say and hence to estimate a Value-at-Risk for a given confidence level for this

loss type, assuming that the probability distribution has the form set out

above.

,

say and hence to estimate a Value-at-Risk for a given confidence level for this

loss type, assuming that the probability distribution has the form set out

above.

We note that  for

for

to

correspond to a probability density function, so:

to

correspond to a probability density function, so:

Suppose the  losses,

losses,

,

are assumed to be independent draws from a distribution with probability

density function and

suppose

,

are assumed to be independent draws from a distribution with probability

density function and

suppose  of

these losses are less

of

these losses are less  and

and

are

greater than .

The likelihood is then:

are

greater than .

The likelihood is then:

This will be maximised for some value that has  ,

i.e. has at

least as large as

,

i.e. has at

least as large as  .

In such circumstances the likelihood is maximised when the log likelihood is

maximised which will be when

.

In such circumstances the likelihood is maximised when the log likelihood is

maximised which will be when  ,

i.e. when

,

i.e. when  ,

i.e. when:

,

i.e. when:

(assuming  and

and

)

)

For these values of and

the

log likelihood is then:

In most circumstances this will be maximised when is

as small as possible, provided is

still at least as large as so

the maximum likelihood estimators are:

However, it is occasionally necessary to consider the case

where we select a  and

have and/or

equal

to zero.

and

have and/or

equal

to zero.

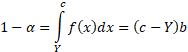

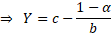

To estimate a VaR at a confidence level  we

need to find the value

we

need to find the value  for

which the loss is expected to exceed only

for

which the loss is expected to exceed only

%

of the time, i.e. such

that (if

%

of the time, i.e. such

that (if  ):

):

A similar approach can be used for tri-uniform distributions

or other more complex piecewise uniform distributions.

Somewhat more complex is if takes

the form of a triangular distribution, i.e. where:

where  are

all constant.

are

all constant.

Nguyen

and McLachlan (2016), when developing a new algorithm for maximum

likelihood estimation of triangular or more general polygonal distributions,

note that in the case where  and

and

then

Oliver (1972), “A maximum likelihood oddity”, American Statistician 26, 43–44, indicates

that

then

Oliver (1972), “A maximum likelihood oddity”, American Statistician 26, 43–44, indicates

that  for

some

for

some  and

moreover that if the sample is ordered so that

and

moreover that if the sample is ordered so that  then

then

where:

where:

Asymptotically, on average, the number of observations in  appears

to be approximately two.

appears

to be approximately two.

We can apply this reasoning to the more general triangular

distribution where we do not know by

again noting that in many cases the log-likelihood will be minimised by setting

to

be as small as possible, provided is

still at least as large as ,

and then separately handling cases where the likelihood can be improved by

selecting a higher value for .