Portfolio Backtesting

4b. Testing backtest quality

statistically: Fitting ‘period by ‘period’

[this page | pdf | references | back links]

Return to Abstract

and Contents

Next page

4.6 Commonly, we

want the model not only to fit the data in aggregate but also to fit it ‘period

by period’. By this we mean that we want exceptionally adverse outcomes to

occur apparently randomly through time rather than being strongly clumped together

into narrow time windows. The latter might imperil the solvency of a firm more

than the former, since there would be less time during such a window to

generate new profits or raise new capital needed to maintain a solvent status

or credible business model.

4.7 Campbell

(2006) explains that the problem of determining whether a ‘hit’ sequence

(i.e. for, say, VaR, an indicator of the form  which is 1 if the

actual outcome for time period

which is 1 if the

actual outcome for time period  is worse than the

is worse than the  -quantile VaR, and 0 otherwise) is acceptable involves two key properties, namely:

-quantile VaR, and 0 otherwise) is acceptable involves two key properties, namely:

(a) unconditional

coverage, i.e. actual probability of occurrence when averaged through time

should match expected probability of occurrence; and

(b) independence, i.e. that any two elements of the hit sequence should be independent of each

other.

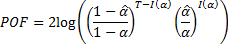

4.8 The former

can be tested for by using, for example, Kupiec’s (1995)

test statistic as described in Campbell

(2006), which involves a proportion of failures  ,

defined as follows, where there are

,

defined as follows, where there are  observations:

observations:

where  = observed number of

failures,

= observed number of

failures,

4.9 Alternatively

it can be tested for by using a z-statistic also described in Campbell

(2006):

4.10 Campbell

(2006) also describes several ways of testing for independence, including Chrisftofferson’s

(1998) Markov test (which examines whether the likelihood of a VaR

violation at time depends on whether or

not a VaR violation occurred at time  by building up a

contingency table). This idea could presumably be extended to correlations

between times further apart. He also describes a more recent test suggested by Christofferson

and Pelletier (2004) which uses the insight that if VaR violations are

independent of each other then the amount of time between them should also be

independent, which hristofferson and Pelletier apparently argue may be a more

powerful test than the Markov test. Campbell

(2006) also describes ways of testing for unconditional coverage and

independence simultaneously.

by building up a

contingency table). This idea could presumably be extended to correlations

between times further apart. He also describes a more recent test suggested by Christofferson

and Pelletier (2004) which uses the insight that if VaR violations are

independent of each other then the amount of time between them should also be

independent, which hristofferson and Pelletier apparently argue may be a more

powerful test than the Markov test. Campbell

(2006) also describes ways of testing for unconditional coverage and

independence simultaneously.

NAVIGATION LINKS

Contents | Prev | Next