Marginal Value-at-Risk (Marginal VaR)

when underlying distribution is multivariate normal

[this page | pdf | back links]

Suppose we have a set of  risk factors

which we can characterise by an -dimensional

vector

risk factors

which we can characterise by an -dimensional

vector  . Suppose that

the (active) exposures we have to these factors are characterised by another -dimensional

vector,

. Suppose that

the (active) exposures we have to these factors are characterised by another -dimensional

vector,  . Then the aggregate

exposure is

. Then the aggregate

exposure is  .

.

The Tail Value-at-Risk,  , of the

portfolio of exposures

, of the

portfolio of exposures  at confidence

level

at confidence

level  , is defined as

the value such that

, is defined as

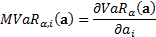

the value such that  . The Marginal

Value-at-Risk,

. The Marginal

Value-at-Risk,  , is the

sensitivity of to a small change

in

, is the

sensitivity of to a small change

in  ’th exposure,

i.e.:

’th exposure,

i.e.:

In the case where the risk factors are multivariate normally

distributed with mean  and covariance

matrix

and covariance

matrix  whose elements

are

whose elements

are  we have the

following.

we have the

following.

As  we have

we have  where

where  is the standard

deviation of the volatility of the (active) portfolio return, otherwise known

if we are focusing on active exposures as the (ex-ante) tracking error.

is the standard

deviation of the volatility of the (active) portfolio return, otherwise known

if we are focusing on active exposures as the (ex-ante) tracking error.

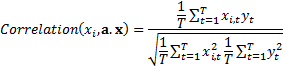

The last part of this equation can be expressed in terms of

the correlation between  and as follows.

Suppose we view the as corresponding

to time series

and as follows.

Suppose we view the as corresponding

to time series  with

with  elements

(which without loss of generality can be assumed to be de-meaned, i.e. to have

their means set to zero) and as corresponding

to a time series

elements

(which without loss of generality can be assumed to be de-meaned, i.e. to have

their means set to zero) and as corresponding

to a time series  . Then the

correlation between and would be

(ignoring any small sample adjustment):

. Then the

correlation between and would be

(ignoring any small sample adjustment):

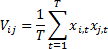

We would also have:

As risks arising from individual positions interact there is

no universally agreed way of subdividing the overall risk into contributions

from individual positions. However, a commonly used way is to define the Contribution

to Value-at-Risk,  , of the ’th

position,

, of the ’th

position,  to be as

follows:

to be as

follows:

Conveniently the then sum to the

overall VaR:

The property that the contributions to risk add to the total

risk is a generic feature of any risk measure that is (first-order)

homogeneous, a property that Value-at-Risk exhibits.