Showing that a Gaussian copula is not in

general an Archimdean copula

[this page | pdf | back links]

An  -dimensional Archimedean

copula is one that can

be represented by:

-dimensional Archimedean

copula is one that can

be represented by:

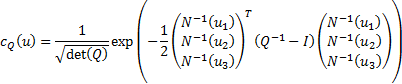

One way of showing that the Gaussian copula is not in

general an Archimedean copula is to consider a three dimensional Gaussian

copula. Its copula density (for a correlation matrix  )

can be written as:

)

can be written as:

In general,  will have 3

different off-diagonal elements, derived from the three different correlations

between

will have 3

different off-diagonal elements, derived from the three different correlations

between  and

and  , between and

, between and  and between and respectively.

Thus the form of the copula density if

and between and respectively.

Thus the form of the copula density if  expressed as

a function of the remaining two components of

expressed as

a function of the remaining two components of  ,

i.e. here and , will differ

from its form if

,

i.e. here and , will differ

from its form if  expressed as

a function of and etc.

However, to be Archimedean, the copula needs to be indifferent between the

components of .

expressed as

a function of and etc.

However, to be Archimedean, the copula needs to be indifferent between the

components of .

For  , the

Gaussian copula has too many free parameters to be Archimedean.

, the

Gaussian copula has too many free parameters to be Archimedean.

Conversely, if returns are multivariate normal and have an

exchangeable copula then the returns can be characterised by a factor structure

involving a single factor.

A set of  random

variables,

random

variables,  (

( )

is said to possess a factor structure if their covariance matrix,

)

is said to possess a factor structure if their covariance matrix,  ,

is of the form

,

is of the form  where is

an

where is

an  matrix,

matrix,  is

an

is

an  matrix (and

there are

matrix (and

there are  factors) and

factors) and

is a

diagonal matrix. Suppose the variance of each is

is a

diagonal matrix. Suppose the variance of each is  and we

define

and we

define  . Then

. Then  have unit

variance and their covariance (now also correlation) matrix also has the form

have unit

variance and their covariance (now also correlation) matrix also has the form  . The copulas

describing the and are the

same. If it is exchangeable and are

multivariate normal then we must have

. The copulas

describing the and are the

same. If it is exchangeable and are

multivariate normal then we must have  being the

same for all

being the

same for all  , say

, say  . This arises

if we set and as

follows, if

. This arises

if we set and as

follows, if  is the

identity matrix:

is the

identity matrix: